REFERRAL PERKS®

Earn $100* for you and your friend for every successful referral.

Whether it’s to start a home renovation, consolidate your debt, or pay for unexpected expenses, borrowing money can be a useful tool to reach your goals. While borrowing does come with costs, knowing what to expect can go a long way towards improving your overall financial well-being.

To help you navigate this, we've created a comprehensive guide that covers what you need to know about borrowing money to meet your financial goals — along with practical tips to help you make decisions about your money.

Before we explore the different types of loans available, let’s go over some fundamental aspects of borrowing. The ‘cost of borrowing’ refers to the original amount that you borrowed, plus interest and any applicable fees you’re required to pay.

Now, let’s take a closer look at some key terms for a deeper understanding of the cost of borrowing.

This is the initial sum you borrow, and it serves as the basis for calculating the total cost of borrowing. For example, if you borrowed $5,000 for a car loan, this would be your principal amount.

Loans either have fixed or variable interest rates. As the name implies, fixed rates don't change for the term of the loan, so your monthly payments stay the same. Variable rates fluctuate with market conditions, so they can increase or decrease over time.

Your repayment terms specify the timeline and schedule to pay back the funds you borrowed. Shorter terms mean higher monthly payments but less interest overall, while longer terms mean lower monthly payments with more interest.

Secured loans are backed by collateral so they pose a reduced risk to lenders, while unsecured loans aren't. Secured loans usually have lower interest rates, but failing to pay can put that collateral at risk. Unsecured loans generally come with higher interest rates to reflect the higher risk.

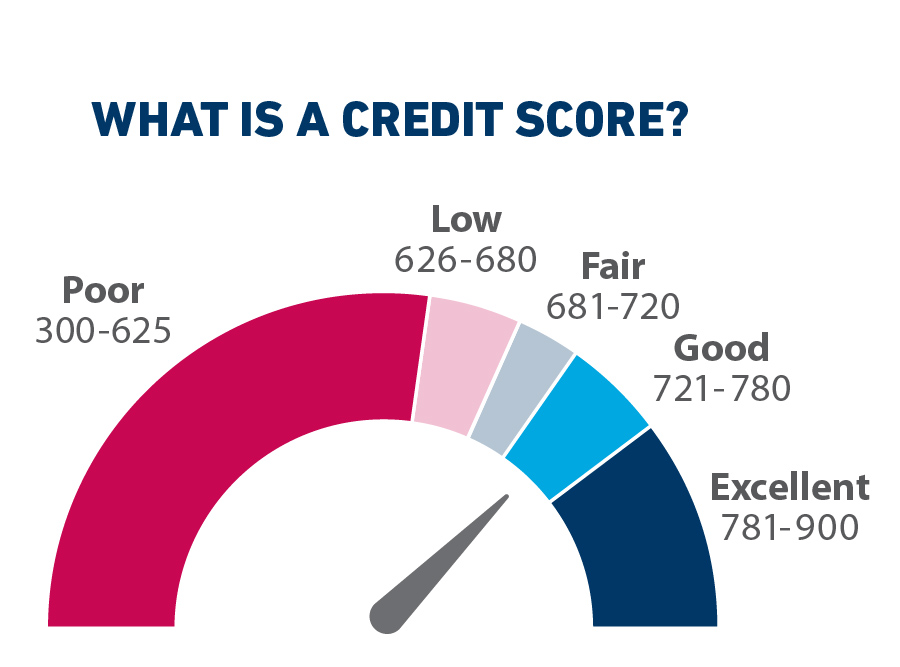

Your credit score is a reflection of your borrowing behaviours distilled into a triple digit number. This number tells lenders how trustworthy of a borrower you are, and can impact the rates you qualify for on your mortgage, personal loans, and more. Typically, the higher your credit score, the lower the borrowing costs. Actions such as paying bills on time, only borrowing what you need, and infrequently applying for credit can help you maintain a stronger credit score.

Regularly checking your credit scores will help you catch errors quicker and stay eligible for better rates. You can request a copy from one of the two major credit bureaus in Canada: Equifax and TransUnion.

As mentioned earlier, establishing yourself as a responsible borrower comes with several perks. Here are just a few key ones:

There isn’t one single way to borrow money. Knowing the different types of loans available can help you choose the option that best fits your unique financial goals and needs.

Resist the urge to borrow excessively. Only take out a loan for the amount necessary.

Be aware of all fees associated with the loan, including late payment penalties and other charges. Read your agreements carefully to know these costs beforehand and avoid headaches down the road.

When it comes to borrowing, your credit score matters. Ignoring it could mean higher interest rates or even rejected applications but nurturing it could mean better terms and interest rates.

Speak to an advisor on the phone or at a branch.

We acknowledge that we have the privilege of doing business on the traditional and unceded territory of First Nations communities.